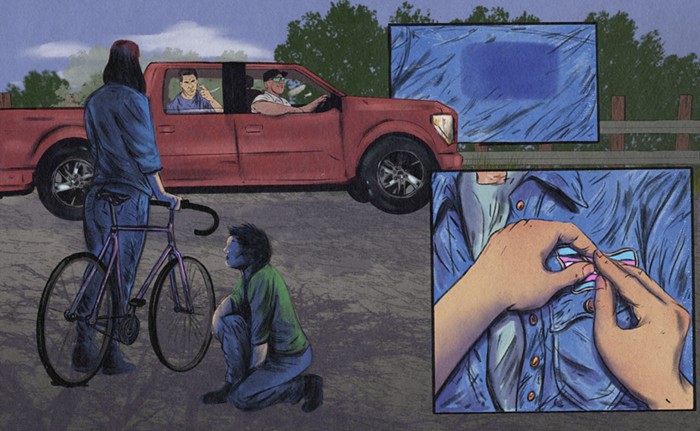

- Jeremy (in red) attempts to pay rent on his bank-owned house

On January 25, grassroots organizing group Standing Against Foreclosure and Eviction demonstrated outside of Wells Fargo in downtown Seattle. Fifteen people shouted and held signs demanding that the bank accept rent in lieu of mortgage from Jeremy Griffin, whose home was foreclosed in November 2012. Metal gates came down and the bank locked up for the day, with six guards and another six bored and irritated SPD officers blocking the entrance.

So, other than the obvious anger surrounding massive foreclosures nationwide, why picket Wells Fargo, why focus on this foreclosure? Because Griffin has a steady job and is ready to pay a mortgage again. But now, with shredded credit, he can't get financing to buy back his house.

Home prices in Washington State have been on the rise. Foreclosures dropped significantly in 2012, due to new legislation, and due to bank settlements over rapacious practices like robosigning. But in 2013, foreclosures are projected to spike again, across the country. In February of this year, Washington was among the worst in the nation for foreclosures. According to RealtyTrac, 1 in 656 houses received notice, compared to a 1 in 849 nationwide average.

One problem for lenders, for Griffin and over three million other families foreclosed on since 2008, is that these houses aren’t worth much. Griffin bought his South Park fixer-upper for $220,000, and according to Zillow.com, it’s now worth only $150,000.

The first industry to pull the emergency brake in 2008 was construction. Despite contracts scheduled a year out, the iron working company Griffin owned went tits up almost immediately; banks stopped lending money to potential developers in November 2008. He laid everyone off. He turned to the Iron Workers Local 86 for contract gigs. When construction picked up in 2011, Griffin had the income to back-pay the delinquent mortgage. But it was too late, he says. “At that point they would only accept total payment. They wouldn’t accept half or part, they said, ‘You have to come with the full amount that you’re late or we’re foreclosing on you. I just couldn’t do it.”

I spoke to the co-founder and partner in the family of businesses associated with Northwest Trustee Services, which mediates foreclosures with borrowers and lenders all over the Western US. It's a vertically integrated foreclosure machine that serves clients with legal counsel, titling, advertising, publication and even newspapers, which print mandatory foreclosure notices at a fraction of the cost of traditional papers: everything you need to execute a foreclosure without going through the court system. Although his business thrives on tragedy, Stephen Routh was charming and helpful on the phone. He said, "The mindset for every employee in the enterprise is that the most successful outcome is if the borrower stays in their home." He even offered to look into Griffin's case to make sure that Griffin's eviction was being put off while a buy-back deal is negotiated with Deutsche Bank, the current title holder.

"There are a lot of moving pieces," said Routh of the shuffling relationships between owners, borrowers, and securities, and the strict timelines for notices and eviction. "The reality is that the borrower has to pay their loan," he said, "There are lots of opportunities, such as forbearance, to keep borrowers in their home." But it's easy for delinquent borrowers to fall through the cracks, even when they are ready to make good on their loan.

Griffin told me he pursued such options, and as for the other side of the story, I couldn't find much, other than a terse statement from Wells Fargo saying he refused relocation assistance. The situation is shitty, because he was the very model of a middle class citizen: a small business owner making a long-term investment in property. At the protest, Griffin told me. "I bought well within my means in a dilapidated part of the city with the idea that I would live there for 20 years and fix it up. Since I was 21, I've been working 40-50 hours a week. I could afford the house—I make $40 an hour. I just needed to be employed."

With so many bank-owned properties on the market, construction, the industry that would keep Griffin in his home, is at a disadvantage. But more worrisome is the present tense. No bank is going to finance a purchase with his history. With the help of allies from SAFE, he is now trying to get into a bank-tenant agreement while he repairs his credit. But he faces down more struggle in advance of the April deadline, explaining by email that such an agreement, where he would rent his house from Deutsche Bank, is uncommon for the real estate clearinghouse. SAFE plans to continue actions, up to an eviction blockade, where protesters will crowd the lawn, lock themselves to stair rails, and otherwise physically prevent the police from throwing Griffin out.